통계 이야기

data mining, forward + backward + ridge + lasso + pcr + pls

728x90

반응형

linear model

Y=β_0+β_1 X_1+…+β_p X_p+ϵ (Least squares methods)

Forward Stepwise Selection

- Best subset selection은 2^p개의 model을 고려해야하므로 p가 크면 사용하기 힘듦

- Null model에서 시작하여 한번에 한 개씩의 explanatory variable을 추가함

Backward Stepwise Selection

- Full model에서 시작하여 한번에 한 개씩의 explanatory variable을 제외함

To choose a model with a low test error

1. estimate test error indirectly by making an adjustment to the training error

ex) C_p, AIC, BIC and adjusted R^2

2. estimate the test error directly using CV approach

- C_p=1/n(RSS+2kσ ̂^2) where RSS: RSS on a training data

- AIC=-2lnL ̂+2k=nln(RSS/n)+2k where L ̂: maximum value of the likelihood

- BIC=-2lnL ̂+kln(n)=nln(RSS/n)+kln(n)

(변수 개수가 많은 model에 더 심한 penalty를 부여하여 AIC보다 더 작은 크기의 model선택)

- Adjusted R^2=1-(RSS/(n-k-1))/(TSS/(n-1)) (R^2=1-RSS/TSS)

(변수가 많아 지면서 RSS가 감소하므로 더 작은 값으로 나누어 R^2 값을 감소시킴)

K-fold CV

- In the past, with large p and/or large n,

- C_p, AIC, BIC, and adjusted R^2 were more attractive approaches for choosing among a set of models

- K-fold CV is a very attractive approach for choosing among a set of models

Ridge regrssion

- ridge regression coefficient estimates β ̂^R

- β_j (j=1,…,p)의 제곱 합으로 penalty를 주기 때문에 전체적으로 β_j를 수축 (shrinkage)시키는 효과가 발생 (intercept β_0는 제외)

- tuning parameter λ(≥0) 가 0일 때는 ridge regression coefficient는 least squares estimate과 같게 되지만 λ→∞에 따라 coefficient는 0으로 수렴하게 됨

- tuning parameter λ는 k-fold CV로 결정

- Least squares estimates은 explanatory variable 의 scale에 영향을 받지 않지만 ridge regression coefficient는 penalty term때문에 explanatory variable의 scale의 크게 의존

- Ridge regression fitting전에 explanatory variable을 standardization할 필요가 있음 (SE로 나누어 줌)

Lasso regrssion

- lasso coefficient estimates β ̂^L

- ridge regression의 단점은 β_j 의 값을 수축시키지만 정확하게 0을 만들지 못한다는 점인데 lasso는 coefficient estimates을 0으로 수축시킴

- tuning parameter λ(≥0) 가 0일 때는 lasso coefficient는 least squares estimate과 같지만 λ가 충분히 크게 되면 모든 coefficient가 0인 null model이 됨

- tuning parameter λ는 k-fold CV로 결정

- Lasso fitting전에 explanatory variable을 standardization할 필요가 있음

PCA

- n × p data matrix X의 dimension을 줄이는 기법

- First PC (PC1): direction of largest sample variance

- Z_1=0.839∗(pop-(pop) ̅ )+0.544∗(ad-(ad) ̅)

- Second PC (PC2) : (1) orthogonal to PC1 (2) again largest sample variance

- Z_1=0.544∗(pop-(pop) ̅ )-0.839∗(ad-(ad) ̅)

- Third PC (PC3) : (1) orthogonal to PC1, PC2 (2) again largest sample variance etc.

- First M principal components, Z_1, . . ., Z_M as the predictors in a linear regression model that is fit using least squares

- X_1, . . ., X_p의 변동이 큰 방향들이 Y와 관련이 있는 방향이라 가정한다면 least squares을 Z_1, . . ., Z_M에 적합하는 것이 X_1, . . ., X_p에 적합하는 것 보다 더 나을 수 있음

- Most of the information in the data that relates to the response is contained in Z_1, . . ., Z_M, and by estimating only M (<p) coefficients we can mitigate overfitting

- Number of principal components, M, is typically chosen by k-fold CV

- Recommend standardizing each predictor

PLS

- PCR approach involves identifying linear combinations, or directions, that best represent the predictors X_1, . . .,X_p in an unsupervised way

- PLS (partial least squares) is a supervised alternative to PCR (i.e. response variable Y를 이용하여 X_1, . . .,X_p를 잘 근사할 뿐만 아니라 Y와 관련된 새로운 변수를 생성)

First PLS direction: compute Z_1 by setting each ϕ_j1 equal to the coefficient from the simple linear regression of Y onto X_j à Z_1=∑2_(j=1)^p▒〖ϕ_j1 X_j 〗 (i.e. response variable Y와 가장 강하게 관련 있는 X_j에 가장 높은 가중치를 부여)

- Second PLS direction: take residuals by regressing each variable on Z_1 and then compute Z_2 using this orthogonalized data in the same as Z_1 was computed based on the original data (X_j의 residuals은 Z_1에 의해 설명되지 않고 남아 있는 정보로 해석 가능)

- Repeated M times to identify multiple PLS components Z_1, . . ., Z_M

- Number M of partial least squares directions used in PLS is a tuning parameter that is typically chosen by k-fold CV

- standardize the predictors and response before performing PLS

#Best subset selection

library(ISLR)

head(Hitters)

dim(Hitters)

sum(is.na(Hitters))

Hitters <- na.omit(Hitters)

dim(Hitters)

library(leaps)

regfit.null <- regsubsets(Salary ~., Hitters)

summary(regfit.null) #변수 총 19개 CRBI가 첫번째 BEST, 두 번째 HIT, ... 8variable/ best만을 뽑는 방법regfit.null <- regsubsets(Salary ~., Hitters, nvmax = 10)

res <- summary(regfit.null)

names(res)

res$rsq #r square

res$bic # 적을수록 좋음

plot(res$rss, xlab = "# of variables", ylab = "RSS", type = "l")

plot(res$adjr2, xlab = "# of variables", ylab = "adj2", type = "l") # 변수 penalty , 어느정도 되면 줄어든다

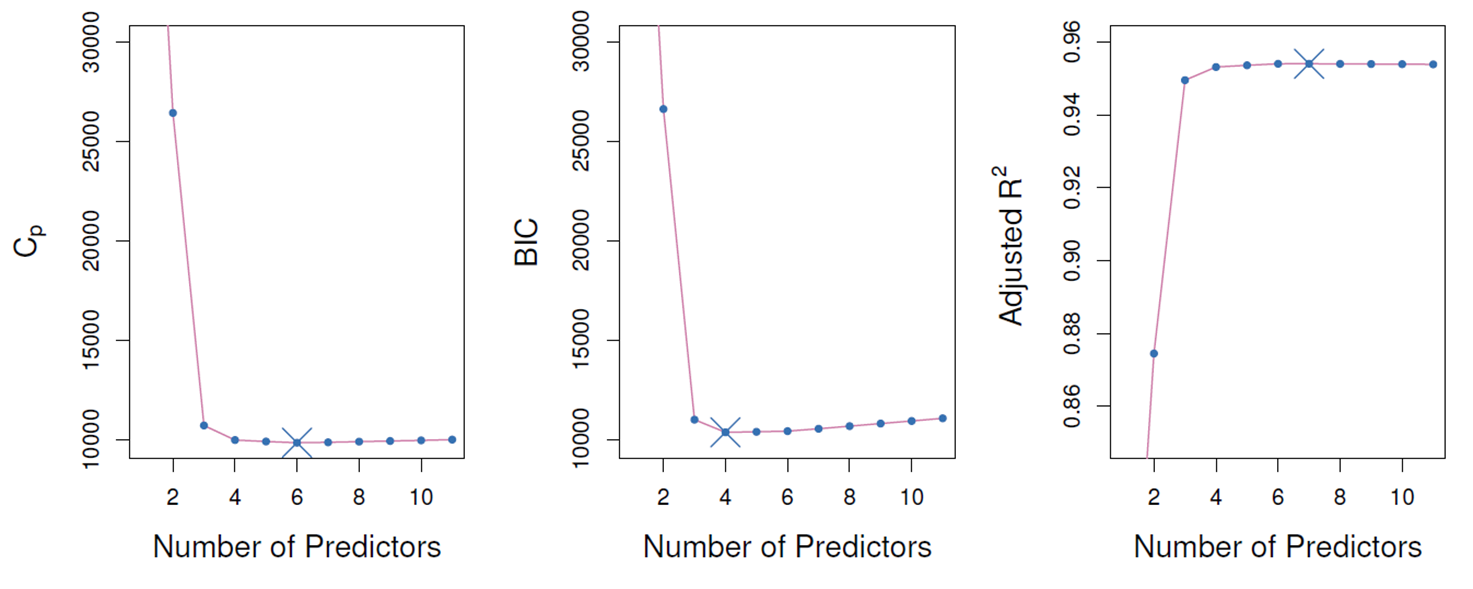

which.max(res$adjr2)

points(10,res$adjr2[10], col = "red", cex= 2,pch =20)

#forward and backward stepwise selection

regfit.fw <- regsubsets(Salary ~., Hitters, nvmax = 19, method = "forward")

summary(regfit.fw)

regfit.bw <- regsubsets(Salary ~., Hitters, nvmax = 19, method = "backward")

summary(regfit.bw)

coef(regfit.null, 7)

coef(regfit.fw, 7)

coef(regfit.bw, 7)# (3) model selection using validation set approach

set.seed(1)

train <- sort(sample(1:nrow(Hitters), 132))

test <- setdiff(1:nrow(Hitters), train)

regfit.best <- regsubsets(Salary~., Hitters[train,], nvmax=19)

test.mat <- model.matrix(Salary~., Hitters[test,])

dim(test.mat)

head(test.mat)

val.error <- rep(NA, 19)

for(i in 1:19){

coefi <- coef(regfit.best, id = i)

pred <- test.mat[, names(coefi)] %*% coefi

val.error[i] <- mean((Hitters$Salary[test]-pred)^2)

}

val.error

which.min(val.error)

regfit.best <- regsubsets(Salary~., Hitters, nvmax= 19)

coef(regfit.best, id = 6) # 이게베스트# (4) model selection using K-fold CV

k <-10

set.seed(1)

folds <- sample(1:k, nrow(Hitters), replace = T)

table(folds)

263/10

cv.errors <- matrix(NA, k, 19, dimnames = list(NULL, paste(1:19)))

cv.errors

j=1

i=1

for(j in 1:k) {

best.fit <- regsubsets(Salary~., data = Hitters[folds!=j,], nvmax = 19)

test.mat <- model.matrix(Salary~., Hitters[folds==j,])

for(i in 1:19){

coefi <- coef(best.fit, id = i)

pred <- test.mat[, names(coefi)] %*% coefi

cv.errors[j, i] <- mean((Hitters$Salary[folds==j]- pred)^2)

}

}

mean.cv.errors <- apply(cv.errors, 2, mean)

mean.cv.errors

plot(mean.cv.errors, type = "b")

which.min(mean.cv.errors)

reg.best <- regsubsets(Salary~., Hitters, nvmax = 19)

coef(reg.best, id =10)

#(5) ridge regression

library(glmnet)

x <- model.matrix(Salary~., Hitters)[,-1]

y <- Hitters$Salary

ridge.mod <- glmnet(x, y, alpha = 0, lambda = 10^seq(10, -2, length=100)) # 알파가 0이면 ridge, 1이면 lasso

coef(ridge.mod)

ridge.mod$lambda[50]

coef(ridge.mod)[,50]

set.seed(1)

dim(Hitters)

train <- sort(sample(1:nrow(Hitters), 132))

test <- setdiff(1:nrow(Hitters), train)

y.test <- y[test]

ridge.mod <- glmnet(x[train, ],y[train], alpha = 0, lambda = 10^seq(10, -2, length = 100))

ridge.pred <- predict(ridge.mod,s =4,newx =x[test,])

mean((ridge.pred - y.test)^2)[1] 139839.6

# select the best lambda using k-fold CV

set.seed(1)

cv.out <- cv.glmnet(x[train,], y[train], alpha=0)

plot(cv.out)

best.lambda <- cv.out$lambda.min

best.lambda

ridge.pred <- predict(ridge.mod, s = best.lambda, newx = x[test,])

mean((ridge.pred-y.test)^2)

out <- glmnet(x, y, alpha = 0)

predict(out, type = "coefficients", s = best.lambda)#(6) lasso

lasso.mod <- glmnet(x[train,], y[train], alpha = 1, lambda = 10^seq(10, -2, length = 100))

plot(lasso.mod)

set.seed(1)

cv.out <- cv.glmnet(x[train,], y[train], alpha = 1)

plot(cv.out)

best.lambda = cv.out$lambda.min

best.lambda

log(best.lambda)

lasso.pred <- predict(lasso.mod, s = best.lambda, newx = x[test,])

mean((lasso.pred-y[test])^2)

out <- glmnet(x, y, alpha = 1)

coef.lasso <- predict(out, type = "coefficients", s = best.lambda)

coef.lasso[coef.lasso != 0]# (7) PCR

library(pls)

library(ISLR)

head(Hitters)

dim(Hitters)

sum(is.na(Hitters))

Hitters <- na.omit(Hitters)

dim(Hitters)

set.seed(1)

train <- sort(sample(1:nrow(Hitters), 132))

test <- setdiff(1:nrow(Hitters), train)

x <- model.matrix(Salary~., Hitters)[,-1]

y <- Hitters$Salary

y.test <- y[test]

#fit PCR with all data

set.seed(2)

pcr.fit <- pcr(Salary~., data = Hitters, scale = T, validation = "CV")

pcr.fit

summary(pcr.fit)

validationplot(pcr.fit, val.type = "MSEP") #MSEP : Prediction에 대한 MSE

#2~3개만 넣어도 상당히 정확하다고 볼 수 있음, 한개 component만 해도 40%정도 설명

#fit PCR with training/test data

set.seed(1)

pcr.fit <- pcr(Salary~., data = Hitters, subset = train, scale = T, validation = "CV")

validationplot(pcr.fit, val.type = "MSEP")

pcr.pred <- predict(pcr.fit, newdata = x[test,], ncomp = 5)

mean((pcr.pred-y.test)^2)

pcr.fit <- pcr(y~x, scale = T, ncomp = 5)

summary(pcr.fit)

#(8) partial least square(PLS) > 변수를 줄이기 위해 변수들 간의 relation이 높은 것 위주로 만드는 것

library(pls)

pls.fit <- plsr(Salary~., data = Hitters, subset = train, scale = T, validation = "CV")

summary(pls.fit) # 감소했다가 증가했다가

validationplot(pls.fit, val.type = "MSEP") #2개에서 거의 최소

pls.pred <- predict(pls.fit, x[test,], ncomp = 3)

mean((pls.pred-y.test)^2)

pls.fit <- plsr(Salary~., data = Hitters, scale = T, ncomp = 3)

summary(pls.fit)

data mining, forward + backward + ridge + lasso + pcr + pls

728x90

반응형

댓글